Capital Flows to Latin America and the Caribbean in five charts: 2023 year-in-review and early 2024 developments

21 Mar 2024

|

Nota informativa

Áreas de trabajo

Latin American and Caribbean international bond activity in 2023 rebounded from the 2022 lows.

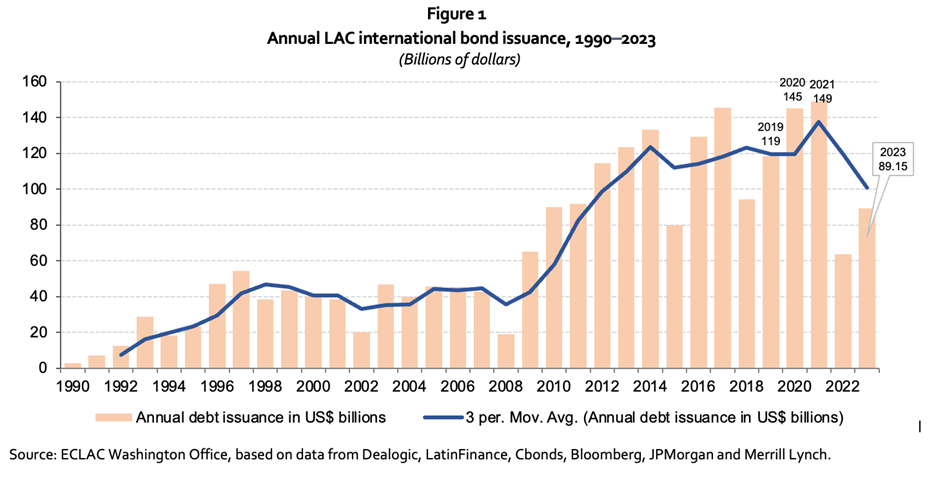

- Latin American and Caribbean (LAC) issuers placed US$ 89 billion of bonds in international markets in 2023. This total was 40% higher than in 2022 but 35% lower than the average issuance in the three year period from 2019 to 2021 (figure 1).

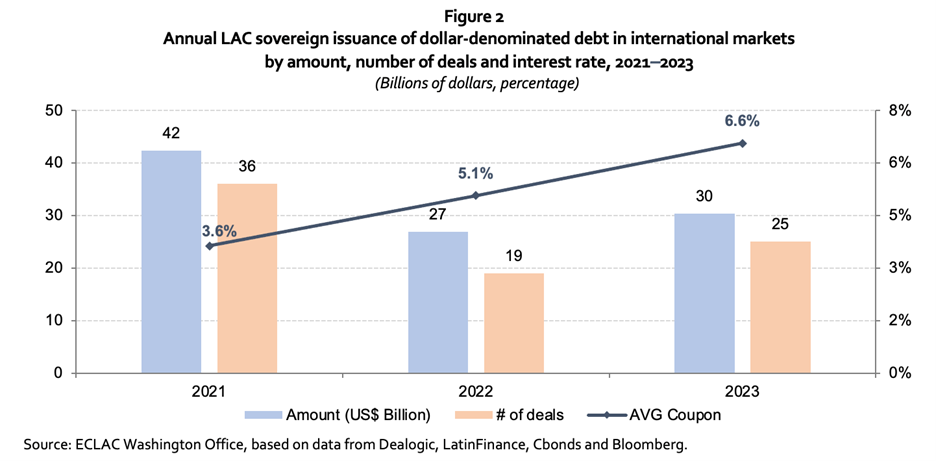

- The average coupon on the region’s international bond issuances in the in 2023 was 1.65 percentage points higher than in 2022. Illustrating how the region’s borrowing costs have increased, the average coupon rates on dollar-denominated sovereign issuances have climbed from 3.6% in 2021 to 6.6% in 2023 (figure 2).

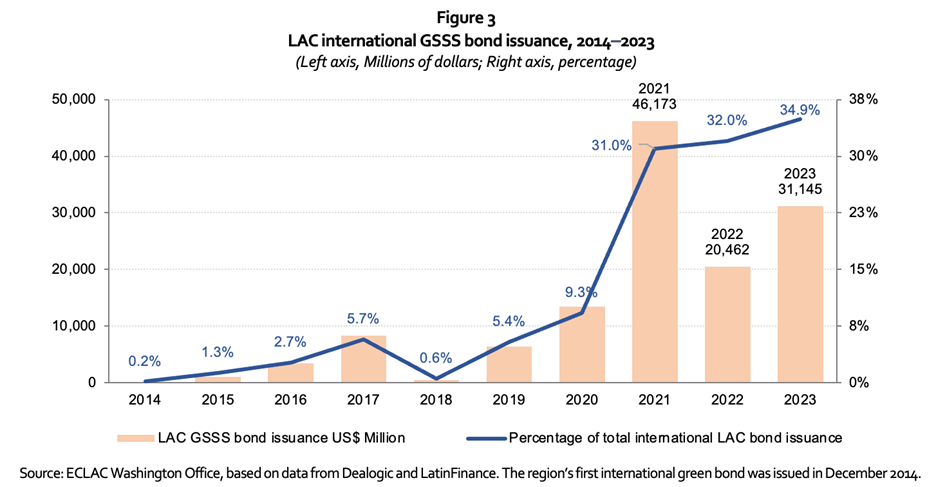

- The region’s issuance of international green, social, sustainability and sustainability-linked (GSSS) bonds reached US$ 31 billion in 2023, up 52% from 2022, but with an average coupon that was 2.1 percentage points higher. This total represented a record 35% share of the region’s total annual issuance in international markets (figure 3).

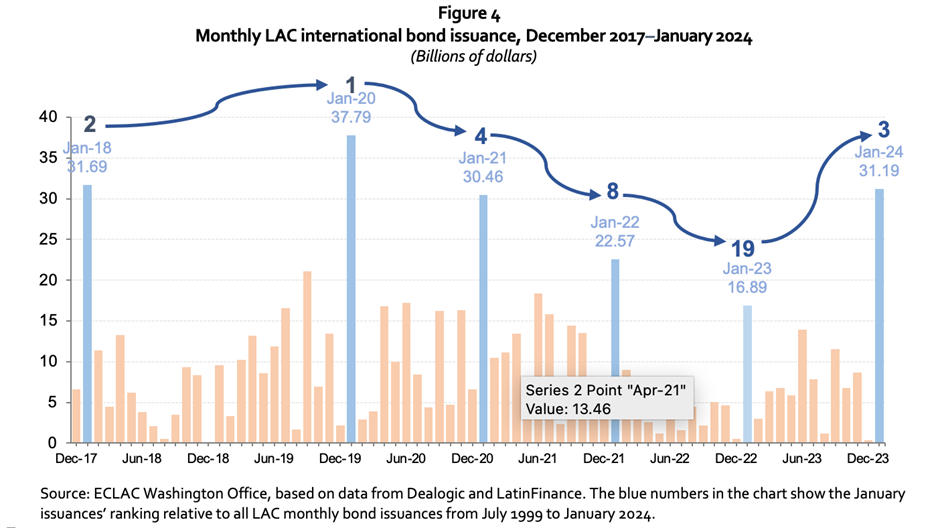

- The region’s international bond issuances are off to a strong start in 2024. In January 2024, LAC governments and companies placed the region’s third highest ever monthly amount of debt in international markets (US$ 31.2 billion) (figure 4).

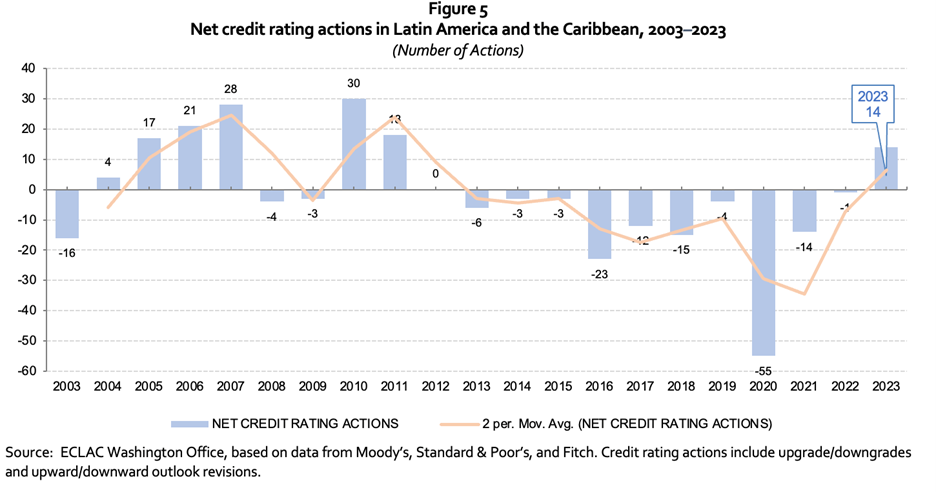

- Following ten consecutive years when negative credit rating actions outnumbered positive actions in the region, in 2023 there was a net positive balance of fourteen more positive actions than negative. It is the best balance since 2011 (figure 5).

For a complete and detailed analysis see the PDF attachment with the full document.

Link:

Sede(s) subregional(es) y oficina(s)

País(es)

-

Estados Unidos

Estados Unidos